Grid Software: Modernizing a grid under strain

Introduction

The electric grid is the backbone of the global economy, powering industries, cities, and homes around the world. In the U.S. alone, the grid serves more than 150 million customers across over 6 million miles of transmission and distribution lines. But this vast network, much of it decades old, is buckling under unprecedented stress. Traditional strategies, focused on more capital expenditure (capex) and infrastructure buildouts, can’t keep up with accelerating energy demand or weakening asset resiliency.

At Energize, we see this moment as a significant turning point. For the first time, multiple forces are colliding to reshape the grid: AI-driven data center growth, scaling onshore manufacturing, and large-scale electrification are driving historic demand, just as aging assets, wildfire risk, and rising congestion expose deep vulnerabilities. The industry’s default to construction is no longer enough. What’s needed is a smarter, more flexible grid—one that layers digital intelligence on top of physical assets to stretch capacity, improve reliability, and accelerate decarbonization.

In our latest Deep Dive, we explore the evolving grid software landscape: how this opportunity came to be, where the most promising digital solutions are taking hold, and what it really takes for startups to scale in the utility ecosystem.

Access the full report here.

Under Pressure: Challenges Facing Today’s Energy Infrastructure

Aging Physical Assets

The U.S. grid is aging quickly. The average transmission line is 40 years old, and the average transformer is 38 years old. In both cases, much of the infrastructure is already at or nearing the end of its design life, and by 2040, more than 100,000 miles of transmission lines will need replacement.

This means the grid requires investment—a lot of it. Between 2024 and 2030, U.S. grid investment is expected to rise from ~$80 billion annually to over $100 billion, with an increasing share flowing into the distribution system. But more capex brings its own consequences. Utilities pass costs to customers, and average retail electricity rates have already climbed 28% since 2018.

Worse, resiliency and reliability are slipping. Grid-caused wildfires more than tripled between 2018 and 2024, while the average U.S. customer outage grew from 5.8 hours in 2022 to 8.4 hours in 2024—a ~45% increase.

As a result, utilities are stuck in a difficult cycle. They must invest in replacing and upgrading aged infrastructure, but projects are delayed by permitting hurdles and supply chain bottlenecks. Consumers, meanwhile, are paying higher rates while facing more frequent wildfires, blackouts, and service interruptions. Capex-heavy approaches alone cannot keep pace with mounting challenges to grid reliability, resiliency, and demand—and the costs are ultimately borne by the consumer.

Surging Congestion and Interconnection Bottlenecks

For the first time in decades, U.S. electricity demand is scaling rapidly—in many cases faster than utilities can supply. The rise of AI data centers, EVs, and broader electrification is expected to drive a 25% increase in demand between 2023 and 2030.

The grid is already showing strain. Congestion costs exceeded $20 billion in 2022, with the heaviest impacts in ERCOT and CAISO. And even as renewable generation sites are being built farther from major load centers, the number of new transmission miles has declined, leaving the system unable to move low-cost power to where it’s needed most.

Limited transmission capacity is also driving a historic backlog in new project interconnections. U.S. interconnection queues grew from approximately 450 GW in 2010 to more than 2,200 GW in 2024. Without sufficient infrastructure, projects stall in queues, unable to deliver power even as demand accelerates. Utilities and grid operators face a dual challenge: relieve today’s congestion while also planning the future system that can absorb tomorrow’s supply.

Grid Capacity Underutilization

Despite these factors, the grid is also starkly underutilized. Conservative line ratings, coupled with outdated power flow management, have led to load levels that fall well below what infrastructure could safely deliver.

In an effort to safeguard reliability, utilities design the grid under an “N-1” contingency assumption—ensuring it can operate normally even if a critical component fails. In practice, this means transmission line ratings are set far below their true physical capacity from the outset, “baking in” wide safety margins that reduce usable capacity by 10–50%, depending on geography, system design, and real-time conditions.

Energy deployment across the grid is also highly variable, swinging sharply between peak and off-peak demand. While transmission ratings set a ceiling for peak usage, power lines typically operate around a 50% load factor—carrying only about half their peak load on average. These load fluctuations, once considered inevitable, have intensified with the rise of intermittent generation from renewables, broader electrification, and more frequent extreme weather events that drive heating and cooling spikes.

As variability increases, utilities must navigate the tension between reliability and efficiency—preserving safety margins while making better use of existing infrastructure. Balancing these competing pressures will determine how effectively the grid can meet the accelerating demands of a rapidly electrifying economy.

The Grid Software Opportunity

The challenges outlined above share a common thread: they can’t be solved by construction alone. For decades, the utility playbook has been to add more steel to the ground: more lines, substations, and transformers. But today’s realities demand more than capex; they demand adaptability, speed, and intelligence.

This is where software comes in. Rather than building or replacing physical assets, software layers digital intelligence on top of them, unlocking hidden capacity, improving reliability, and accelerating planning cycles. By serving as the connective tissue of the modern grid, software can stretch the value of existing infrastructure while enabling utilities to meet rising demand more cost-effectively and resiliently.

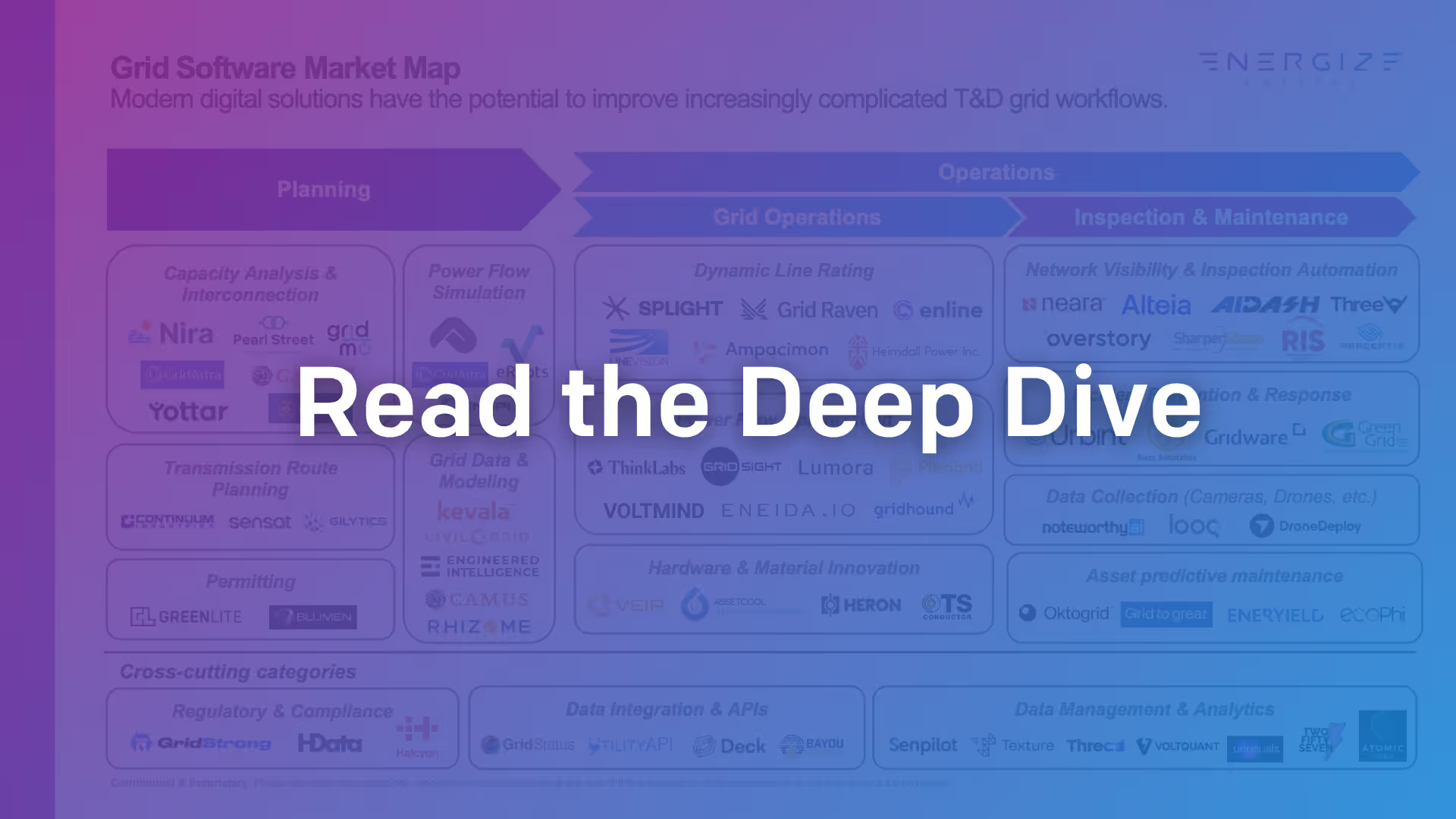

Several digital technologies are poised to address modern grid challenges:

Grid Interconnection: Unlocking Stalled Supply

Software is bringing clarity and speed to one of the grid’s most complex bottlenecks: connecting new projects to the grid.

Part of the challenge in managing grid congestion and interconnection processes is the difficulty in understanding true current-state grid conditions (including required upgrades) and coordinating stakeholders across asset developers, utilities, and system operators. Software, provided by upstarts like Nira Energy, can manage this complexity, providing visibility into the impact of new asset deployments on power flows and driving stakeholder alignment in interconnection submissions.

Grid Operations and Planning: Improving Utilization

Software enables operators to see and manage the grid dynamically, unlocking utilization and capacity.

The first step in better leveraging existing grid infrastructure is making sense of the data flowing from assets and networks. By aggregating and analyzing this information, software from companies like Gridsight or ThinkLabs builds a real-time picture of grid operations, highlighting stress points and inefficiencies. This intelligence enables planning and operations teams to anticipate challenges, optimize utilization, and strengthen overall system performance.

Inspection and Maintenance: Extending Asset Life

Software is transforming inspections from reactive compliance to proactive resilience, extending system longevity and reducing capex requirements.

Digital tools can integrate data from sources such as drone imagery, LiDAR, and sensor networks to provide actionable insight into grid condition and upgrade planning. With predictive analytics, software like Neara or Buzz Solutions enables utilities to prioritize the highest-impact maintenance and replacement projects, while solutions like GridStrong are working to automate compliance to align systems with regulatory requirements. These tools accelerate time-to-value on capital investments and improve overall grid resilience.

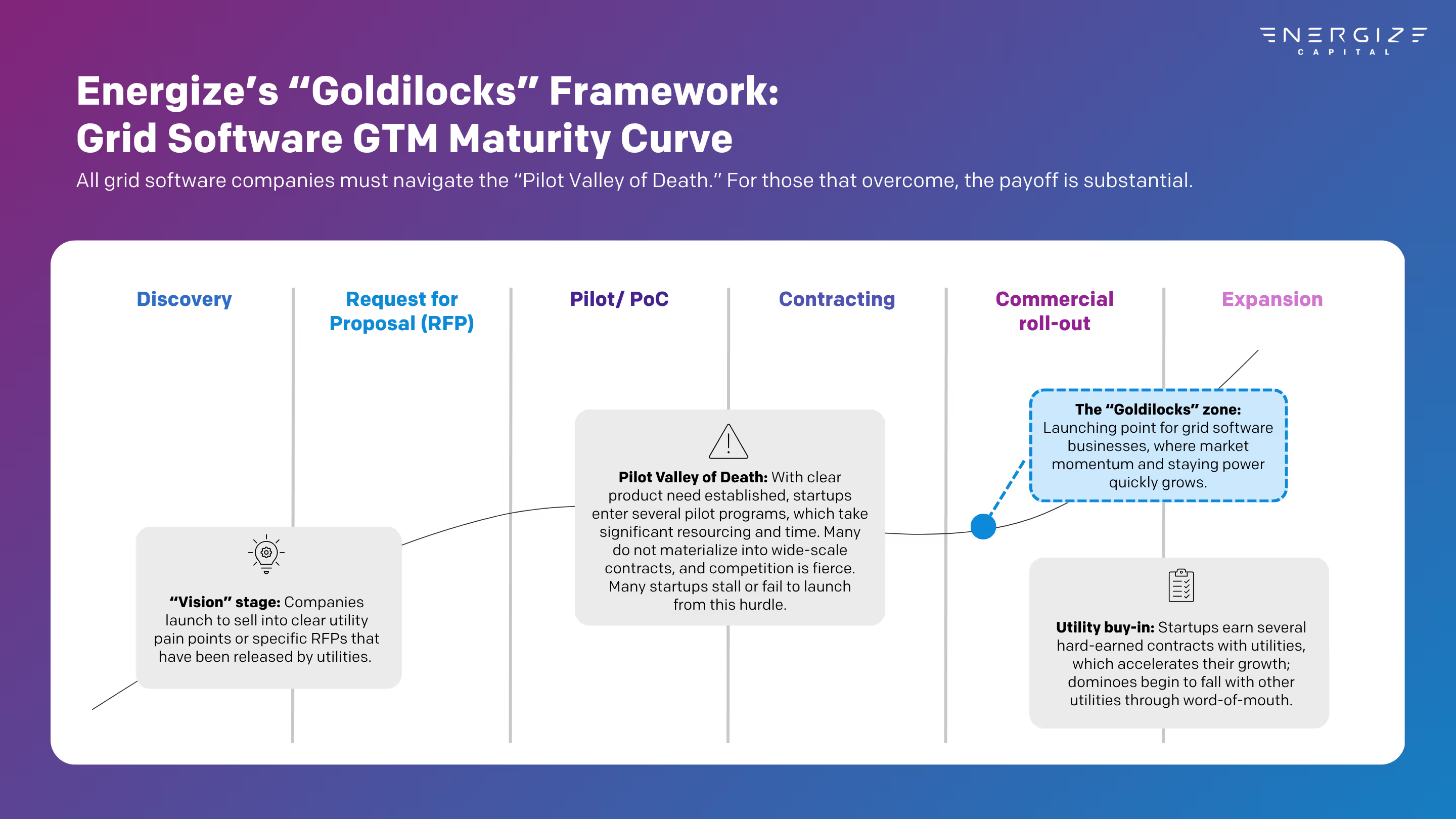

Finding the “Goldilocks Zone”: Strategies for Building Scale as a Grid Software Company

Despite strong demand and clear opportunity, grid software companies often struggle to reach commercial scale. The core challenge lies in selling to utilities, a process commonly described as the “Utility Pilot Valley of Death.” Even with growing interest in digital tools, utilities remain slow to adopt new processes. Startups can spend two to five years navigating pilots, RFPs, and layers of red tape before securing a single commercial agreement. For many, the imbalance between heavy upfront investment and limited early revenue proves insurmountable.

But for those that survive, the payoff is enormous. Contracts can scale into the tens of millions of dollars, and once a company lands its first one or two utility deals, momentum compounds as word of mouth spreads across the sector. This is the grid software “Goldilocks Zone” —a stage of accelerating commercial traction with utilities that lays the foundation for durable, entrenched businesses.

Here are four recurring trends from businesses that have successfully navigated the “Pilot Valley of Death”:

1. Balance focus with scale: Anchor the solution to well-defined budget line items within the utility—ideally those outside innovation budgets, which often operate in silos. Begin with a focused, single business-unit use case as a wedge, then expand by leveraging early relationships to build broader utility buy-in and increase contract value over time.

Example: AI-driven risk management platform Urbint partners with the operations units of utilities, often beginning with a single product that serves as a wedge into broader applications within that business line. Its partnership with National Grid started with a focus on damage prevention before expanding to additional operational use cases.

2. Leverage trusted relationships: Collaborate with service providers and consultants that already hold long-standing utility relationships. Their credibility accelerates adoption and opens access to bigger utility budgets.

Example: Predictive modeling platform Neara partnered with utility services leader Osmose to combine advanced network modeling with field data collection and structural analysis. This collaboration drives adoption and helps utilities improve grid resiliency and optimize maintenance efforts through more accurate, data-driven asset decisions.

3. Stay flexible on business models: Adapt go-to-market and delivery models to meet utilities where they are—whether by layering in services or integrating hardware (e.g., sensors) to unlock procurement pathways often closed to pure SaaS offerings.

Example: Gridware combines intelligent sensors with analytics software to deliver grid monitoring and wildfire prevention solutions, illustrating how hybrid models can unlock new budgets and accelerate adoption within utilities.

4. Prioritize efficiency and endurance: Given the long sales cycles and uneven growth patterns in the utility sector, disciplined capital allocation and operational resilience are critical. Companies that maintain controlled burn rates and a scrappy, resourceful commercial approach are best positioned to endure and compound value over time.

Example: Nira Energy exemplifies this approach. After raising initial funding through Y Combinator, the company bootstrapped to profitability, scaling sustainably to meet the complex and evolving needs of energy customers.

Conclusion

The U.S. grid is at a breaking point. Traditional infrastructure spending alone cannot keep pace with accelerating demand or mounting reliability risks, and without new approaches, it will only grow more costly, inefficient, and fragile. While software isn’t the silver bullet, it is the force multiplier that can stretch existing assets, cut costs, and accelerate the energy transition.

For startups and investors, the challenge is navigating the slow-moving utility sector without burning out. But for those that hit the Goldilocks zone—balanced growth, efficiency, and partnerships—the outcome isn’t only big contracts. It’s building the digital nervous system of the future grid, the backbone of our economy.

Building in the space? We'd love to hear from you. Reach out to me on LinkedIn here.

Recent News & Insights

Let’s Build What’s Next